Recruitment factoring and agency cash flow

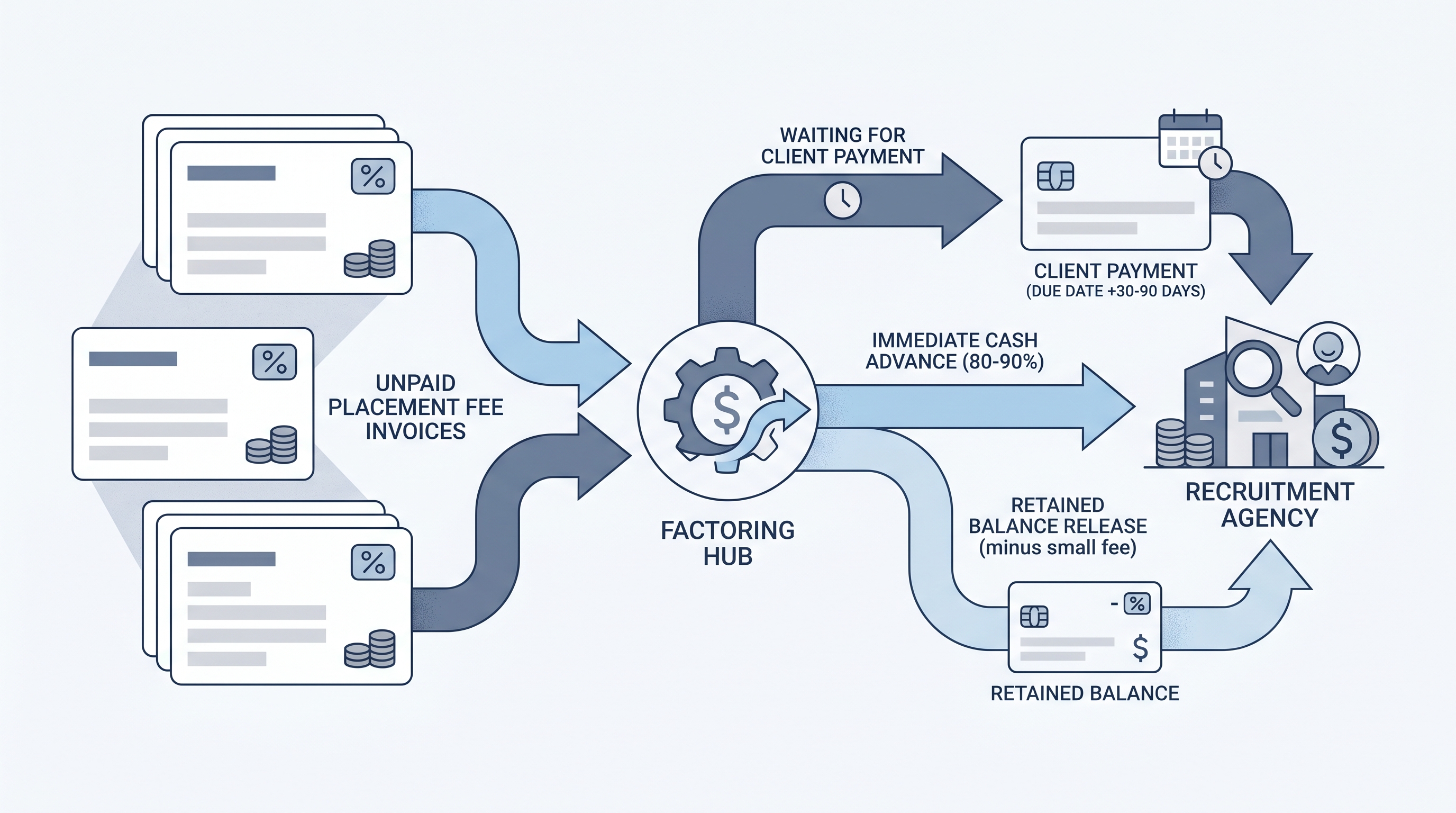

Invoice factoring for recruitment agencies is a financing arrangement where an agency sells outstanding placement fee invoices to a third-party funder at a small discount, receiving most of the cash within 24 to 48 hours rather than waiting 30 to 90 days for the client to pay.

Michal Juhas · Last reviewed May 8, 2026

What is recruitment factoring and agency cash flow?

Invoice factoring is a short-term cashflow tool used by recruitment and staffing agencies to convert unpaid placement fee invoices into working capital without waiting for clients to pay. An agency sells an outstanding invoice to a factoring company at a small discount, receives most of the cash within 24 to 48 hours, and the factor then collects payment directly from the client when the invoice falls due.

For a contingency recruitment agency billing a 25 percent fee on a placed candidate at an 80,000 salary, a single invoice represents 20,000 of revenue sitting unpaid for 30 to 90 days. Multiply that across several active placements with enterprise clients on extended payment terms and the working capital gap becomes a real operational constraint, limiting the ability to hire additional recruiters, invest in sourcing tools, or sustain a marketing pipeline while searches are underway.

Factoring is not debt: the agency is selling an asset it already owns, the right to receive payment on a confirmed invoice, in exchange for immediate liquidity. The factoring fee, typically 1 to 5 percent of invoice value, is the cost of accelerating that cash. Whether factoring makes financial sense depends on whether the revenue velocity it unlocks outweighs the fee cost over time.

In practice

- A boutique IT recruitment agency places three candidates with an enterprise client on Net 60 terms in the same month. The combined fees represent 45,000 of confirmed revenue, but payroll falls in two weeks. Rather than drawing down a personal overdraft, the founder submits the three invoices to a factoring company, receives an 85 percent advance within 48 hours, and continues hiring without the cashflow squeeze.

- A staffing agency operations manager reviewing payment analytics notices that two large clients account for 70 percent of outstanding receivables and consistently pay between day 55 and day 75 on Net 45 contracts. She uses this data to negotiate Net 30 terms on new engagements with both clients, reducing structural reliance on factoring over the following quarter.

- An agency founder evaluating a factoring proposal notes that the factor requires a notification clause disclosing to clients that the invoice has been assigned. After reviewing existing master services agreements with two enterprise accounts and finding no assignment restrictions, she proceeds, but first confirms the clause wording with her commercial lawyer to avoid triggering consent requirements with clients that have stricter contract governance.

Quick read, then how hiring teams use it

This page is for recruitment agency founders, finance leads, and operations managers who need to understand how factoring works, when it makes sense, and what risks it introduces. TA leaders who engage recruitment agencies will also find the client-side implications useful for understanding how payment behaviour affects supplier relationships.

Plain-language summary

- What it means for you: Factoring lets you turn a confirmed but unpaid placement invoice into working capital within 48 hours, at a cost of 1 to 5 percent of the invoice value.

- How you would use it: Submit an invoice you are waiting on to a factoring company, receive most of the cash upfront, and let the factor collect from the client when the due date arrives.

- How to get started: Compare two or three specialist recruitment factoring providers on advance rate, fee structure, recourse versus non-recourse terms, and whether client notification is required. Run one invoice through as a test before committing to a full facility.

- When it is a good time: When you have a large confirmed placement invoice, a client with good credit but long payment terms, and an immediate working capital need that a bank overdraft cannot cover quickly enough.

When you are running live reqs and tools

- What it means for you: Factoring is a cashflow lever, not a substitute for sound payment term negotiation. The agencies that use it most effectively combine factoring for short-term peaks with systematic improvements to contract terms and collections processes that reduce structural dependence on it over time.

- When it is a good time: When a large placement fee at Net 60 or Net 90 is creating an operational constraint in the same month, and the revenue opportunity from staying fully staffed or funded outweighs the 1 to 5 percent fee.

- How to use it: Factor selectively on large invoices from creditworthy clients where the advance unlocks a specific operational benefit. Automate invoice reminders and accounts-receivable tracking using workflow automation to shorten collection cycles on invoices you do not factor.

- How to get started: Calculate your average days to actual payment receipt across your last 20 invoices. If the gap consistently exceeds your contract terms, tighten collections first before adding a factoring cost layer. If payment timing is genuinely unpredictable due to client procurement processes rather than late payment, factoring on large invoices is a rational tool.

- What to watch for: Guarantee period exposure during the advance window, recourse obligations if a client defaults, and assignment restriction clauses in existing client contracts. Read rebate and clawback clauses on placement fees and master services agreements for recruitment agencies before committing to a factoring facility.

Where we talk about this

On AI with Michal live sessions, agency cashflow and commercial structure topics come up in the AI in recruiting track when agency founders and TA operations leads discuss how to systematize the business side of running a search firm alongside sourcing and screening automation. The Sourcing Lab cohort covers placement fee structures, retainer agreements, and contract governance so TA leaders and agency principals can align on vocabulary and operational process.

Around the web (opinions and rabbit holes)

Third-party creators cover invoice factoring and agency cashflow from financial, operational, and sector-specific perspectives. These are starting points, not endorsements. Verify any factoring arrangement with a qualified accountant or commercial finance broker before committing.

YouTube

- Invoice factoring explained for small businesses covers the mechanics of how factoring works, the cost structure, and how to evaluate whether it makes sense versus alternative financing.

- Staffing agency cash flow management covers the specific dynamics of recruitment and staffing cashflow, including payroll funding, invoice timing, and growth financing.

- Recourse vs non-recourse factoring covers the credit risk differences between the two structures and which environments suit each approach.

- Factoring invoices in r/RecruitmentAgencies covers real practitioner accounts of using factoring facilities to manage cashflow in a growing agency.

- Invoice financing options in r/smallbusiness covers comparisons between factoring, invoice discounting, and overdraft facilities from small business operators.

- Staffing agency financing in r/Entrepreneur covers how staffing and service businesses fund growth before revenue normalizes.

Quora

- How do staffing agencies manage cash flow when clients pay late? collects practitioner perspectives on factoring, overdraft facilities, and payment term negotiation from agency owners.

Factoring versus alternative cashflow tools

| Aspect | Invoice factoring | Bank overdraft | Retainer upfront |

|---|---|---|---|

| Speed to cash | 24 to 48 hours | Immediate (if facility exists) | On engagement signing |

| Cost | 1 to 5% of invoice | Interest on drawdown (usually lower) | No direct cost |

| Scales with revenue | Yes, per invoice | No, fixed limit | No, per engagement |

| Credit risk | Recourse: agency. Non-recourse: factor | Agency | Agency |

| Client visibility | Required with some factors | None | None |

| Best for | Large invoices, Net 60 or Net 90 clients | Routine shortfalls with existing banking | Retained and executive search |

Related on this site

- Glossary: Agency invoice payment terms and collections, Rebate and clawback clauses on placement fees, Master services agreement for recruitment agencies

- Glossary: Backfill and replacement guarantees, Agency escrow and retainer, Workflow automation

- Glossary: Recruitment agency software, Human-in-the-loop

- Workshops: Sourcing Lab

- Course: Starting with AI: the foundations in recruiting

- Membership: Become a member